Janet Yellen chimed in over the weekend that an inflation overshoot will be good, though she didn’t elaborate on exactly why that is. The Fed and the markets seem to agree with her. As we approach this Thursday’s consumer inflation report, treasury bond yields are down while near-term inflation expectations are stable. Some of the people who are not joining this government-sponsored kumbaya though are Larry Summers and Bill Dudley. These gentlemen are letting everyone know that the economy could be over-heating and we are going to have an inflation problem - if we don’t do something right away. The inflation problem they are referring to is a recession that could happen if inflation goes out of control and the Fed is forced to raise interest rates to cool things down.

We don’t have a crystal ball to say who is right, but a lot may depend on just how large the inflation spike is going to be. The upcoming inflation report will shed some light on the matter, but my hunch is that the June report is going to be more illuminating. Unfortunately that’s not expected till July, so this is what we will have for the time being.

The economist surveys expect May inflation to come in at about 4.8% (all rates annualized). Looking under the hood of this survey though, I think there could be issues. The same survey had forecast a rate of 2.4% for April which turned out to be completely wrong - actual inflation came in at 9%. I am willing to believe that 9% was too high and possibly an outlier, but there is a risk that 4.8% is too low. A lot of the data I have seen in the last two weeks seems to indicate that price pressures are growing stronger rather than weaker. Wages grew at 6% annualized in May as per last Friday’s jobs report. That was higher than the 2.5% estimated by economists while the overall jobs numbers came out below estimates. That sounds like a stagflationary pressure, similar to my view a month ago. Construction jobs actually declined because they can neither find materials nor workers. The US ISM1 Manufacturing report for May had this to say:

Record-long lead times, wide-scale shortages of critical basic materials, rising commodities prices and difficulties in transporting products are continuing to affect all segments of the manufacturing economy. Worker absenteeism, short-term shutdowns due to part shortages, and difficulties in filling open positions continue to be issues that limit manufacturing-growth potential.

Interestingly, the ISM people copy-pasted the above paragraph verbatim from their April report.

Meanwhile May auto sales came in strong but missed estimates because they cannot make cars fast enough due to computer chip supply issues.

Globally, purchasing manager sentiment2 declined across several South-East Asian countries, again due to supply issues. The raw material shortage was reflected in China’s Caixin report too. In their words:

Inflationary pressure was enormous as price gauges continued to rise. Both the measures for input costs and the prices service providers charged rose to their highest points of the year.

Normally I am appropriately skeptical of data coming out of mainland China, but Caixin is so far seen as independent. For example, consider this article and they are still standing.

If the supply and demand pressures are only getting stronger, should analysts expect inflation in May to be just half that in April? It could, if growth is slowing down enough - perversely because of inflation and related shortages. E.g. if the 9% inflation rate in April was enough to put the brakes on growth, yielding lower inflation for May. But if that happened the data enumerated above doesn’t support it. I am able to see some signs of lower than expected growth, but not lower inflation.

It could be that the economists surveyed don’t want to be too far off from Fed or Treasury forecasts. Deferring to the Fed is typically a good thing - most people know (but don’t apply) the old market adage that one shouldn’t fight the Fed. But the Fed actions you don’t want to fight are its open market operations such as QE. Inflation forecasts on the other hand are fair game. After all, the Fed and other government or multilateral entities (such as the Congressional Budget office (CBO), IMF3 etc.) routinely get economic forecasts wrong. This is despite that the Fed not only forecasts inflation but also sets policy - whose express purpose is to influence future inflation!

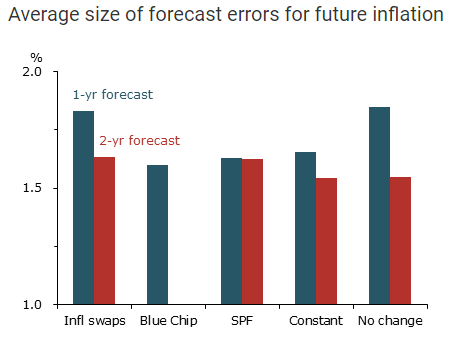

For that matter, private sector forecasts and even market forecasts of inflation are not much better4. Here is an interesting chart from the San Francisco Fed:

On a 2-yr forecast horizon there is basically no meaningful difference between a “no change” forecast and the other sources listed above. Very coyly, the SF Fed did not include the FOMC’s (wildly inaccurate) inflation forecasts in this study!

Anyhow, it is reasonable to be skeptical about whatever the markets, the Fed or private sector economists are forecasting about inflation.

The big question is what should one do to hedge against a rude inflation surprise this Thursday. If the rate blows past estimates, then the narrative is likely to shift towards a high inflation, lower-than-expected-growth world. That’s not good for stocks. It may also place in doubt President Biden’s mega stimulus package which would doubly damage market sentiment. The thin Democratic majorities in Congress are already wobbling.

Given the VIX Index is at a fairly low level of 17 or so, the idea of buying some protection (through VIX futures) may have some merits. One wants to buy protection when it is affordable, not when one has to. What gives me pause though is that naked VIX futures are a bit of a sawed-off shotgun. Collateral damage can happen if things go wrong and I can’t say I like a blatantly pro-inflation bet right now. Is there something more sophisticated? Well, the VIX futures curve is quite steep at present, meaning that buying insurance against market declines a few months in the future is more expensive as compared to the cost of near-term insurance. Could it be a better idea to sell longer-term insurance and use the proceeds to buy near-term insurance?

I like futures more than options because my head hurts when I think of vegas, deltas and rhos. But I can see some options mavens wanting to sell September S&P 500 puts while buying June puts.

If the inflation numbers come out within estimates, or lower, then I can see insurance positions losing. That’s fine, at least by my reckoning. There do exist people who have made a lot of money by buying insurance at the right time and selling it at exorbitant prices. Whole careers rest on such “tail alpha” strategies (e.g. Taleb). But one shouldn’t over-estimate the ability to do that.

The purpose of insurance is primarily protection, to conserve capital in risky times so one can deploy it later.

Get my newsletter in your inbox every week.

Please read important disclaimers here. Your use of these materials is subject to the terms of these disclaimers.

Institute of Supply Management. The ISM report is one of the most reliable and quick reacting macro measures of the U.S. economy.

Similar to above, but for other countries

I wrote a post on the IMF’s forecast failures during covid, just a few months ago

However, private sector forecasters are paid by clients, not tax dollars. It’s quite alright if clients like being entertained with wrong forecasts from banks and asset managers.