Gold and Silver

There is now more evidence in favor of stagflationary pressures. This morning we received retail sales data for May that declined by 1.3% vs April. Even if one excludes the auto sales sector (given the many supply issues), retail sales declined -0.8% while the expectation was +0.4%. On the other hand, the producer price index (PPI)1 increased at a MoM rate of 9.7% (annualized) while the survey expectation was only 6%.

Growth prints are coming out below expectations and inflation prints above expectations. Tooting my own horn a bit, stagflation has been my thesis since the April jobs report (see here).

The public discourse around inflation is wrongly focused on whether it is going to be transitory or long-lasting (see Larry vs Janet). The discussion should be about the size of the inflationary spike and how that would influence stock markets. A large spike can create it’s own reality whether or not inflation turns out to be long-lasting. Unfortunately, the Treasury-Fed axis is under-estimating the size of the spike even if they turn out to be right about it not being permanent2.

Why are they playing it down?

For Janet Yellen the answer is simple. Inflation talk hurts political support for President Biden’s mega spending plans. But why the Fed? Probably because if the Fed says that “bad” inflation is here, the markets may well hear it as an intent to raise rates. But valuations are anchored on the Fed’s earlier pronouncements that rates will stay zero until 2024. If that turns out to be a wrong assumptions, a large correction (if not a meltdown) is very much possible.

The Fed is riding a tiger. A lot depends on stagflationary pressures not being so strong that markets get spooked and an ugly chain of events follows. So far we are OK, with the VIX at a low 17 or so. But I see hints of discomfort in the VIX futures curve:

October volatility is expected at 22.5% vs the 17 level of the VIX right now - a 5.5 point difference. That’s not an insanely high spread, but it is definitely up there.

Meanwhile many commodity prices are rolling over. Since my previous post on agriculturals, it was nice to see cattle, grains, coffee, sugar and orange juice do well, comfortably beating the S&P (thank you Mr. Market). But last week I saw weaknesses appear in various quarters followed by a large decline on Friday. It did make me feel that perhaps an exit should be considered. This happy realization did not happen a moment too soon - aside from beef, most of these futures are down this week.

The decline is a lot worse in the most stagflation-hit market i.e. construction. The lumber rally has ended in tears with prices down 30% in the last three weeks.

There is a moral here about thinly traded markets. It is a good idea to take profits quickly when jitters appear after a long rally. Such jitters are noticeable in the news flow and intra-day jumps in prices. This is the nature of feedback loops in a low liquidity environment. It can also be good to rejoin quickly once the blood-letting abates and green shoots of a new trend are visible.

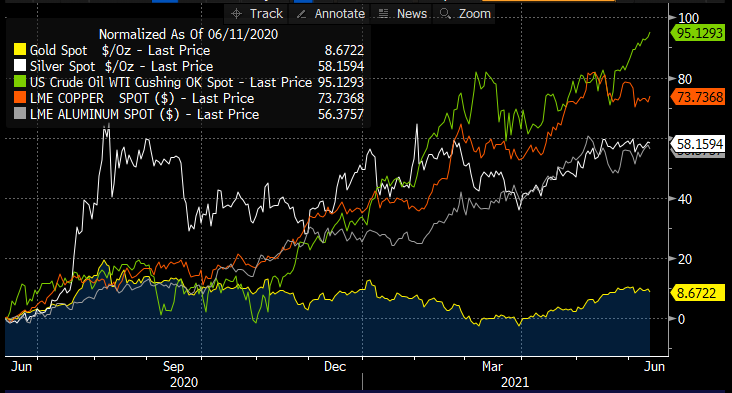

Anyhow, now that “production” commodities like industrial metals and agriculturals are taking a breather, let’s take another look at gold.

Energy and industrial metals have galloped ahead in the previous year, but Gold has not. It is up only 9% despite the recent surge. Silver on the other hand has behaved more like industrial metals, up nearly 60%. This could be because silver has more industrial uses as compared to gold and so it has been riding the growth story.

But what happens if growth runs into stagflation? In that case growth will undershoot, but inflation expectations may continue to rise. Meanwhile, the Fed may stay behind the curve and keep treasury yields low. This would mean that real interest rates3 keep falling.

The price of gold is very closely determined by the level of real rates. When real rates decline, the price of gold goes up and vice versa. Silver prices also do that, though somewhat less predictably. And therein lies a thought. If going forward real rates continue to decline, but growth prospects also reduce, then silver prices may be stagnant or could even decline.

But gold would rise because it is almost exclusively driven by real rates.

There is some additional support for this from the gold/silver cross:

The price of gold in units of silver is about the lowest it has been in the previous 5 years.

If one makes the argument that gold has better prospects than silver in the current conditions and silver is trading at a high level, then it could be reasonable to buy gold and sell silver in the futures market. As precious metals they have some similar drivers which reduces the overall volatility of the trade.

Risk balancing is also an issue to be considered because silver is twice as volatile as gold. Maybe one should want to place just half as many dollars in silver as compared to gold.

Something else I like about this is that there are indications the US economy is moving from raw materials driven inflation to inflation in the price of services. If that is the case, there could be a lot of focus on gold as production commodities may not be seen as a good inflation hedge.

For that matter there could also be a lot of focus on cryptocurrencies to see if they perform well compared to gold.

Should be interesting to see a rematch of that old feud!

Get my newsletter in your inbox every week.

Please read important disclaimers here. Your use of these materials is subject to the terms of these disclaimers.

This is the output PPI which is a weighted average of the prices producers are able to charge for their goods.

I am more in the camp of transitory inflation similar to Yellen.

Here real rates are the difference between treasury bond rates and expected inflation. Specifically, 10 year US treasury yields and 10 year inflation expectations implied by the market prices of Treasury Inflation Protected Securities (TIPS).